/01-shutterstock_1419581063.jpg)

Last updated: April 8, 2026

Do you struggle to keep up with your debts? Debt management is a big concern for many people. Whether you have a good credit history and a high credit score or you’re looking to repair your credit, debt consolidation may be an option to help you pay down your debt and improve your overall financial health. In this blog, discover what debt consolidation is and how to consolidate your debts.

Key Takeaways

- Debt consolidation combines your debts into one monthly payment, making it easier to stay organized.

- It may help lower your interest rate or monthly payment, depending on your credit and loan terms.

- It’s often most useful if you’re dealing with high-interest debt like credit cards.

- It can simplify your finances, but long-term success still depends on your spending and repayment habits.

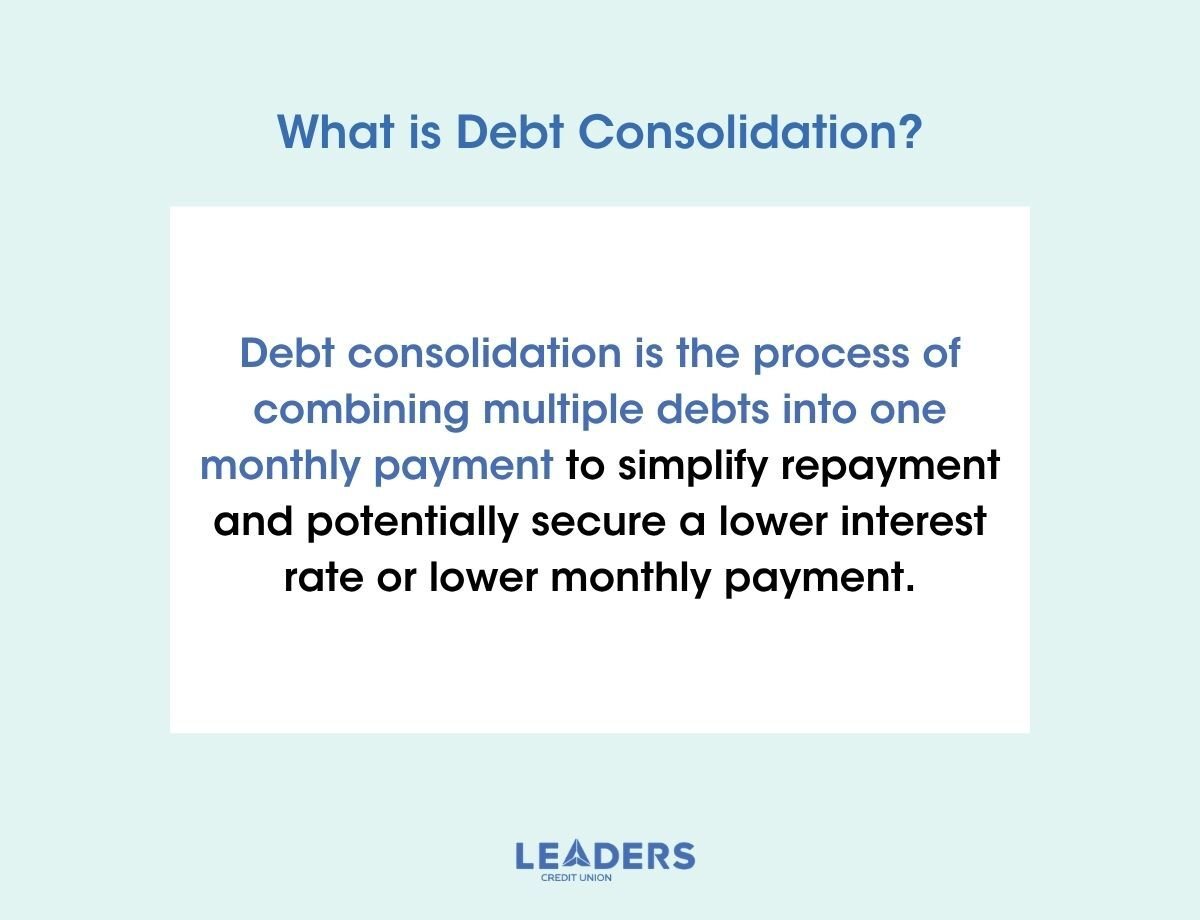

What Is Debt Consolidation?

Debt consolidation is the process of combining multiple debts into one monthly payment, typically through a loan or balance transfer credit card. The goal is to simplify repayment and potentially secure a lower interest rate or lower monthly payment.

One of the main benefits of debt consolidation is the potential to lower your monthly payment. This usually happens if you qualify for a lower interest rate or choose a longer repayment term. However, not everyone will see lower payments, and total interest costs may increase over time.

We’ll review some of the various vehicles for debt consolidation in the next section, but there are a variety of ways to handle debt consolidation if it’s something that will help you.

What Are the Options for Debt Consolidation?

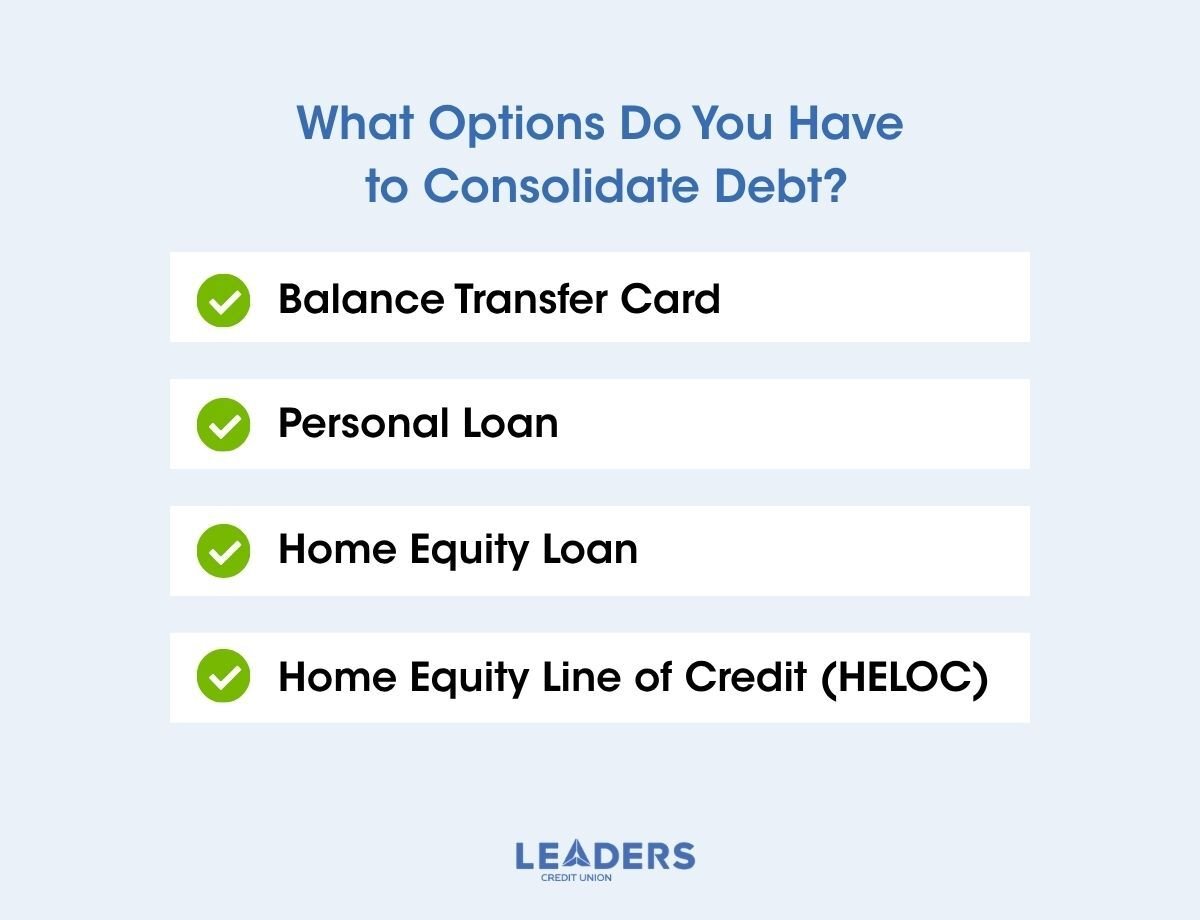

If you’re carrying high-interest debt and you want to save money, you have several options to consolidate your debt.

1. Balance Transfer Card

A balance transfer credit card is a card that allows you to transfer balances from other credit cards and/or loans at a low introductory rate. For example, many balance transfer cards may offer a 0% introductory APR for the first six or 12 months. During that period, you can make payments to reduce the amount of credit card debt, while saving money on interest.

2. Personal Loan

Personal loans may be taken out through a credit union or bank and used to pay off debt. The methodology is different for a loan than it is for a credit card. You would use the money from the loan to pay your creditors. Then, the loan payment would replace your credit card payments and usually at a lower interest rate than what you were paying before.

3. Home Equity Loan

Home equity loans can be used for many purposes, including debt consolidation. With a home equity loan, the equity you have accrued in your house is used as collateral. It’s common for home equity loan interest rates to be affordable, especially if you’re working with a credit union. You’ll use the money from your loan to pay your other creditors, then make regular monthly payments on the new loan.

4. Home Equity Line of Credit

A home equity line of credit (HELOC) is similar to a home equity loan in that it uses the equity in your home as collateral. You’ll pay only for what you withdraw, which gives you some flexibility in paying down debt. You can withdraw what you need to pay your creditors and then repay the financial institution that gave you the HELOC to eliminate your debt.

Pros vs. Cons of Debt Consolidation

While debt consolidation can assist some in their financial journey, it may not be the best decision for everyone. Here's a list of pros and cons to help you consider if it's the right step for you.

Pros

-

Organizes your debts into one payment

-

Could improve credit if payments are made on time

-

Easier to manage month to month

- Could reduce monthly payments

Cons

- Needs good credit for better interest rates

- Could increase total interest for payments if extended

- Paying off can help, but habits need to be built for lasting change

- Could prompt a hard inquiry on your credit score

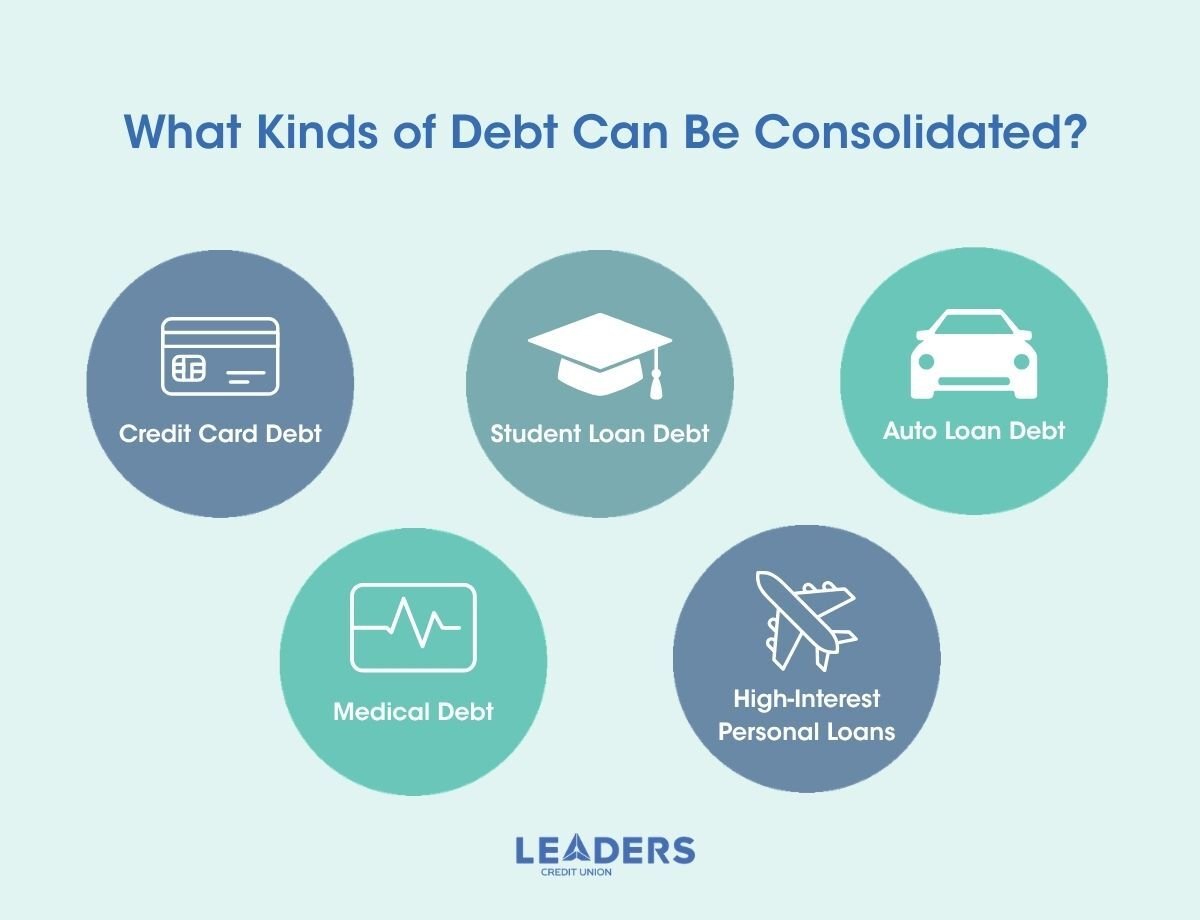

What Kinds of Debt Can Be Consolidated?

One of the most common questions we are asked about loan consolidation is which kinds of debt can be consolidated. The good news here is that if you’re worried about debt payment, you can consolidate many different kinds of debt:

Credit Card Debt

Credit card debt is often consolidated because many people have credit cards with disadvantageous interest rates. If you can qualify for a low or no-interest balance transfer card, you can significantly reduce your monthly payment with consolidation.

Student Loan Debt

Student loan debt can be overwhelming and difficult to pay off with high monthly payments and interest rates. It’s important to know that if you have unpaid interest on federal student loans, the interest will be added to your loan principal.

Auto Loan Debt

If you have a car loan with a high interest rate, you may be able to save money by consolidating the balance into a debt consolidation loan.

Medical Debt

Medical debt is an issue for many Americans and it may come with high interest rates. Consolidating medical debt can help you save money on interest and get out of debt more quickly.

High-Interest Rate Personal Loan Debt

If you’ve previously taken out a personal loan with a high-interest rate, you may be able to consolidate it to lower your monthly payment and pay less interest.

Debt consolidation isn’t the right choice for everybody, but if you have debt with a high-interest rate, it may be worth exploring debt consolidation as an option.

How Does Debt Consolidation Work?

Debt consolidation isn’t complicated, but if you haven’t done it before, you’re probably wondering how it works. Here’s what you need to know.

As we noted above, debt consolidation is the process of taking multiple debts owed to different creditors and combining them into a single monthly payment. You can consolidate debt with a balance transfer credit card, a loan, or a home equity line of credit.

Once you have been approved for your new credit card or loan, you’ll transfer the balance if you’re using a credit card, or use the funds from your loan or HELOC to pay off your other debt. In some cases, you may ask your financial institution to make electronic transfers to pay your debt. In others, you may simply use the funds from your loan to pay your creditors directly.

After you have transferred or paid your debt, you will no longer need to pay those creditors. Instead, you’ll make one monthly payment to either your credit card company or to the financial institution that gave you the loan or line of credit. You’ll have the option of making extra payments if you choose, so you can pay down your debt quickly.

How Can Someone Start the Process of Debt Consolidation?

Here are the steps to follow if you decide that debt consolidation is something you want to do.

1. Decide Which Debt to Consolidate

The first step is to review your debt and decide which debt balances you want to consolidate. As a rule, your best bet is to consolidate any debt with a high-interest rate since debt consolidation usually results in a lower interest rate and a lower monthly payment.

2. Total Your Debt

Next, you’ll need to determine a total amount for your debt consolidation. The amount will help you decide how large a debt consolidation loan you need or how high your limit needs to be on a balance transfer credit card.

3. Check Your Credit Report

Before you apply for a debt consolidation loan or credit card, we recommend getting free copies of your credit reports to review them. Equifax, Experian, and TransUnion all must provide you with a free annual credit report and you may be able to view your report more often if you pay for a credit monitoring service. Leaders members may also check their credit score in their online banking or mobile app.

4. Research Lenders and Credit Cards

We recommend doing your own research to see which lenders or credit card options are available to you. If you’re a Leaders Credit Union member, we suggest that you look at our personal loans, HELOCs, and other products as options. Make sure you read the fine print to understand how long your introductory rate lasts and any associated fees.

5. Apply for Your Loan or Credit Card

After you’ve narrowed your debt consolidation choices, it’s time to apply for a loan or credit card. Keep in mind that you may need to pay an application fee if you’re applying for a loan. Make sure that your application is complete and that you provide all necessary information—and that you answer questions from the underwriting team quickly to avoid delays.

6. Close On Your Loan or Activate Your Credit Card

Once you’re approved for a new credit card or a loan, the next step is to schedule and attend your loan closing or activate your new credit card. You can’t consolidate your debt until you’ve taken this step.

7. Transfer or Pay Your Debts

After closing on your loan or activating your credit card, you’ll need to follow instructions from your lender or credit card company to transfer the debts. In some cases, you may transfer the debt and your lender will pay the balance; in others, you may be the one responsible for using the funds to pay off your debts.

8. Make Monthly Payments

Transferring your debts ends the consolidation process, but you still have a responsibility to make monthly payments for the entire loan term or to make at least your minimum monthly payment on your new credit card.

Is Debt Consolidation Right for You?

Here are a few questions to ask yourself to decide if debt consolidation is right for you:

- Is debt a source of stress for me?

- Has my financial situation improved since I applied for credit cards or loans where I still have debt?

- Would it help me to have fewer debt payments to make each month?

- Is my credit score in a range that will allow me to qualify for debt consolidation?

- If you answered yes to at least three of these questions, then you’re likely to be a good candidate for debt consolidation.

FAQs about Debt Consolidation

Q: What is debt consolidation?

A: Debt consolidation is the process of combining multiple debts into one single monthly payment, often through a loan or balance transfer credit card. Instead of juggling several due dates and interest rates, you make one payment each month. In some cases, consolidation can also lower your interest rate or simplify your payoff plan.

Q: Will debt consolidation really help lower my monthly payments?

A: Yes, debt consolidation can lower your monthly payments, but it depends on your interest rate and loan terms. If you qualify for a lower interest rate or choose a longer repayment term, your monthly payment may go down. However, a longer term can mean paying more in interest over time. Your credit score plays a big role in the rate you’re offered, so better credit usually leads to better savings.

Q: How do I know if it's time to consolidate my debts?

A: It might be time to consider consolidation if you’re having trouble keeping up with multiple payments, carrying high-interest debt (like credit cards), or only making minimum payments each month. It can also help if you feel overwhelmed managing different balances and due dates.

Q: What are some signs that consolidating debt isn't necessary right now?

A: Debt consolidation may not be needed if you only have one debt, your interest rate is already low, or you’re comfortably paying off your balance each month. In those cases, adding a new loan or account might not provide much benefit.

Consolidate Your Debt with Leaders Credit Union

Debt management doesn’t need to be a source of worry. Instead of juggling multiple monthly payments and settling for high interest rates, consider debt consolidation as a way of lowering your interest rate and monthly payment and getting out of debt quickly.

Are you considering debt consolidation? Leaders Credit Union is here to help! Learn more about our personal loans and apply online from the convenience of your home when you’re ready.

Want to learn more about how to handle debt with your spouse? Read our other blog,

Leaders Credit Union is federally insured by the NCUA.