Last updated: May 21, 2026

Being a first-time auto buyer is exciting, but it may also feel a little overwhelming. That’s understandable if you’ve never done it before. You likely have questions about the car-buying process, from which first-time financing options are available to you to the loan application process.

While we can’t help you take a test drive and decide which vehicle to buy, we can help you understand car loan requirements, how the auto loan approval process works, and provide useful information about interest rates for car loans and how they impact financing a car.

Key Takeaways

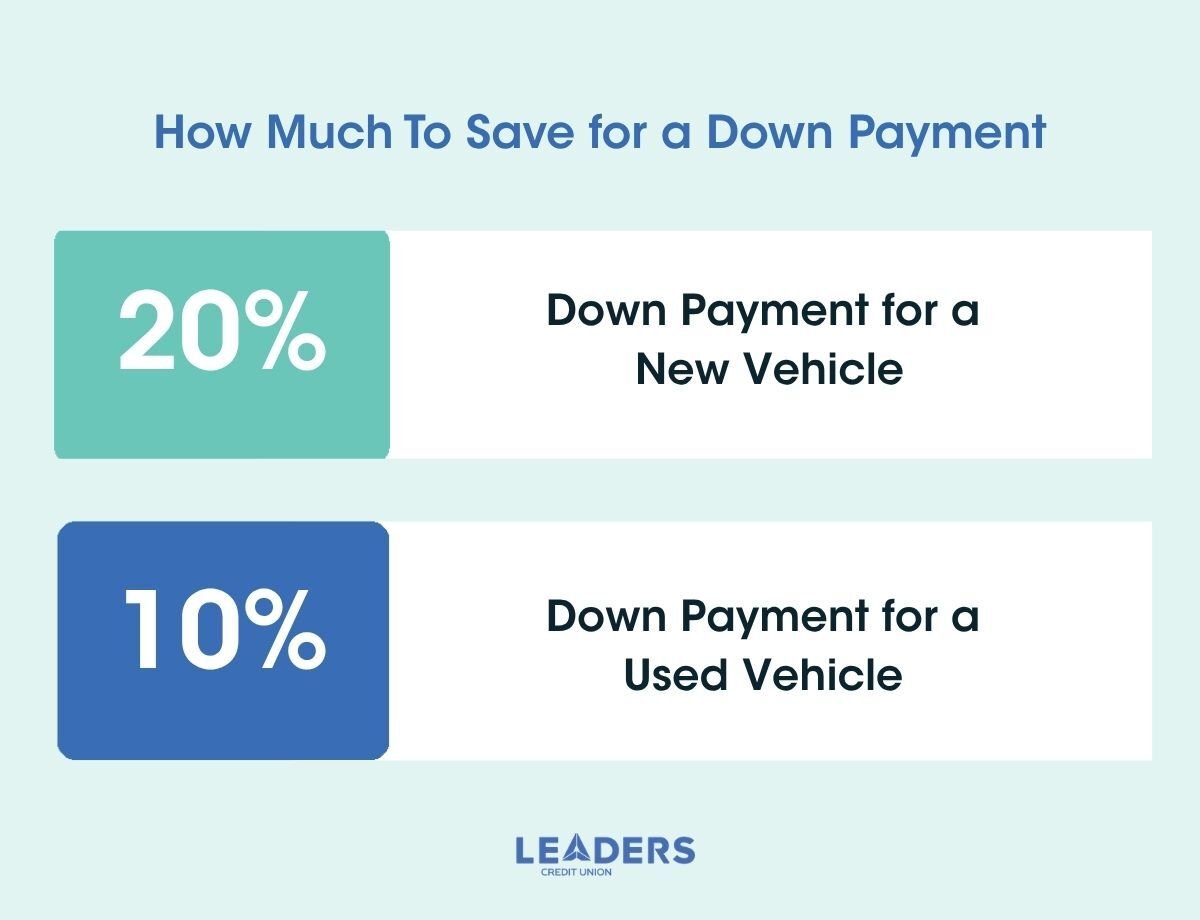

- Aim to save 20% for a down payment for a new car and 10% for a used one.

- Apply for pre-approval and research dealerships to find the best deals.

- Research to find the best interest rates when looking for an auto loan.

- You’ll have more freedom in the long run buying a car than leasing one.

How Much of a Down Payment Do You Need When Buying Your First Car?

The question of down payments can loom large for any first-time car buyer. Here are some down payment tips to help you determine how much you need to save and what impact your down payment will have on your vehicle loan amount.

Our rule of thumb is to make the largest down payment you can afford without negatively affecting your finances. Many experts suggest a 20% down payment for a new vehicle and a 10% down payment for pre-owned inventory. The average price of a new car in 2026 is over $49,000, so that would translate to a down payment between $4,900 and $9,800.

If you can’t afford that much, you can put down less. The main thing to keep in mind is that a larger down payment means borrowing less money. In turn, that means a lower monthly payment and a more advantageous interest rate.

People who can’t afford a 20% down payment may still be able to buy a vehicle. You may have the opportunity to refinance down the line, and you also have the option of making extra payments to reduce the total interest you’ll pay over the term of your loan.

"Buying the right vehicle isn't just about the price, it's about value, reliability, and confidence every time you turn the key," said Trent Taylor, Vice President of Indirect Lending at Leaders Credit Union.

If you're curious about how much you can afford, you can use an auto loan calculator to estimate different payment plans by adjusting down payments, monthly payments, and interest rates. Visit our online finance center to learn more and see if there are any incentives for using digital or online banking or for setting up automatic payments.

What Should First-Time Buyers Know About Car Financing?

First-time car buying tips can help you avoid some of the most common first-time buyer mistakes, which may include things that increase your payments.

-

Decide how much loan payment you can afford each month. It’s important not to overestimate your capacity to pay, which is why we’d suggest creating a household budget if you don’t already have one.

-

Review your credit report for accuracy and identify any potential issues that could affect your credit approval. Examples include late payments and high credit card usage.

-

Apply for pre-approval with several lenders within the same two-week period. Preapproval requires a hard credit inquiry, which will impact your score. If you make all inquiries within the same period, all inquiries will count as a single inquiry, minimizing the impact on your credit score. You’ll also have a better idea of your budget and have something to compare dealership financing offers.

-

Know what to expect when you visit the dealerships. Salespeople and financial representatives will focus on the sticker price, but keep in mind that the out-the-door price is the total you pay and can significantly impact your monthly payment.

-

Learn about your borrowing options. We’ll get into these in more detail in the next section, but it’s a good idea to know what your options are when it comes to loan terms.

If you’re not sure how much you can afford to borrow, our monthly loan payment calculator could help you figure that out.

What Financing Options Are Available for First-Time Car Buyers?

Finding the best car loans for first-time buyers isn’t always easy. Shop around to find the best interest rates, keeping in mind that qualifying for a lower APR will result in a lower monthly car payment.

Financing with a Credit Union or Bank

The first financing option is a new or used auto loan from your credit union or bank. Credit unions typically offer more competitive financing than banks because they pass profits back to their members rather than to shareholders.

In many cases, you could find a flexible loan term ranging from 12 to 96 months. Opting for a longer term may result in lower monthly payments, but you’ll pay more in interest over the term of the loan.

Traditional lenders may also offer features such as loan protection, warranties, and the option to skip a payment if necessary.

Financing with a HELOC

Some people who already own a home may use home equity, either a loan or a line of credit, to buy a new car. It’s rare for a first-time car buyer to already be a homeowner, but if you are, this may be an option for you.

You’ll need a bit of time and patience to find the best car loans for first-time buyers, but it’s worthwhile to do some research to make sure you’re not paying too much.

"Purchasing a vehicle should feel exciting, not stressful, the right guidance makes all the difference," said Trent.

What Are the Pros and Cons of Leasing vs Buying?

Some buyers may not have the money for a down payment on a first car and wonder whether leasing would be a better option. Here are some of the pros and cons of leasing.

Leasing Pros

- Monthly lease payments may be lower than most car loan payments.

- You’ll always be driving a late-model car equipped with the best safety features.

- Some maintenance, including oil changes, may be covered under your lease.

- You don’t need to worry about selling your car; you’ll just turn it in at the end of the lease.

Leasing Cons

- You won’t gain any equity in your leased car.

- If you always lease, you’ll always have a car payment.

- Most leases have mileage limits, and you’ll pay penalties if you go over.

- You’ll still be responsible for some repairs, for example, new tires.

- You may incur additional expenses if your leased car shows excessive wear and tear at turn-in.

As a contrast, here are some of the pros and cons of buying a vehicle.

Buying Pros

- You’ll be building good credit with every payment.

- You can do whatever you want to upgrade your vehicle, something that’s not an option if you lease.

- You can drive as many miles as you want, since there won’t be any mileage restrictions.

- You’ll only need to make car payments for the term of your loan.

- You can sell your car at any time.

Buying Cons

- In the short term, your expenses may be higher than they would be with a lease.

- You’ll be responsible for all repair costs after the warranty expires.

- A significant down payment can take a chunk out of your savings.

- Depending on how long you keep your car, maintenance costs may increase over time.

In the end, it’s really about your money and how you want to spend it. People who want to build equity and have greater freedom to use their vehicle as they wish will likely prefer buying a car to leasing one.

Auto Loan FAQs

What Paperwork Do You Need When Applying for a Car Loan?

You’ll need these documents:

- Proof of identification

- Proof of residence

- Proof of income and employment

- Credit history and payment history

- Details about the vehicle you’re buying

- Proof of auto insurance

- Down payment

How Do Interest Rates Vary for First-Time Buyers?

Interest rates for vehicle loans are based on several factors, including your credit score, payment history, the amount of your down payment, and other factors. If you’re a first-time car buyer and your credit history is limited, you may end up with a higher rate than you would if you had more established credit.

How Can I Improve My Credit Score for a Better Car Loan?

If you want to improve your credit score, start by ordering free credit reports. Review them, and if there are any errors, contact the credit bureaus to correct them. You can improve your score over time by making on-time payments and paying down your outstanding debt to improve your debt-to-income ratio.

How Long Does Car Loan Approval Take?

The typical auto loans approval process may take anywhere from a few hours to several days, depending on the lenders or dealerships. If you submit a complete application with all required paperwork, you could get a quick turnaround time. Some lenders, including Leaders, allow members to apply online and get a quick pre-approval.

FAQs for Financing a Car

Q: How much should I put down for a car loan?

A: For a new car, save at least 20% for your down payment. For a used car, aim for 10%. A bigger down payment means smaller monthly payments.

Q: How can I get the best deal on my auto loan?

A: Get pre-approved and compare offers from multiple lenders and dealerships to find the lowest rate.

Q: Should I buy or lease a car?

A: Leasing costs less upfront, but buying is better for long-term savings and flexibility. When you buy, you own the car and can sell it later.

Q: What are my car financing options?

A: You can get an auto loan from a bank, credit union, or car dealership. Some homeowners may use a home equity line of credit (HELOC).

Find the First-Time Car Loan You Need with Leaders Credit Union

Buying your first car is a big deal, and now you’re armed with information to help. The most important thing you can do is go into the financing process prepared—knowing what you can afford and what to expect.

To help even more, we’ve created The Ultimate First-Time Car Buyer’s Checklist—a free resource to guide you through every step of the journey, from budgeting to getting behind the wheel. You can also read our article, "How to Buy a Car: A Step-By-Step Guide from Pre-Approval to Purchase."

We want you to find the best vehicle loan you can. Explore our car loan options and apply online to get started!

Leaders Credit Union is federally insured by the NCUA.